Key Takeaways

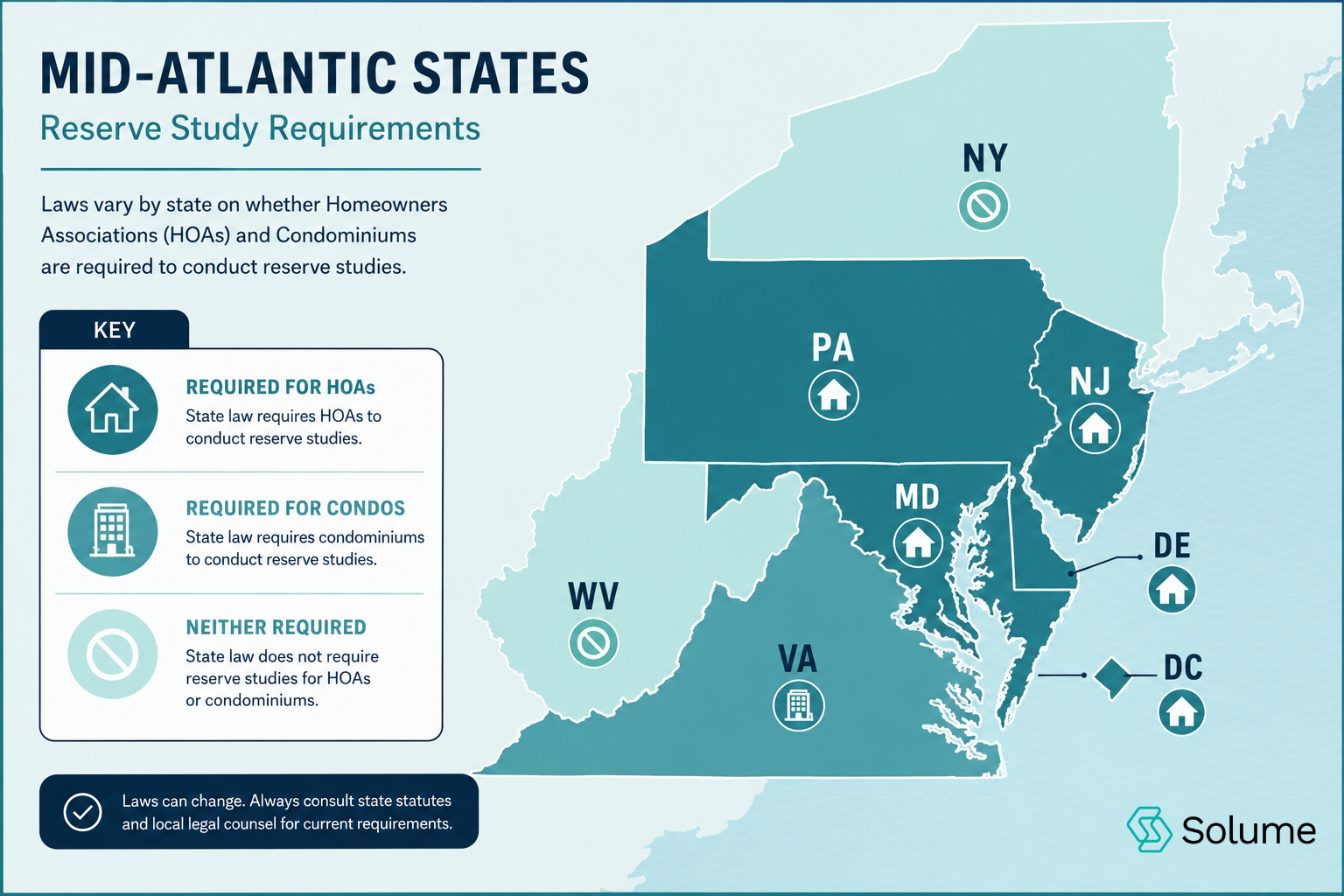

- Virginia HOA Reserve Study Requirements differ by structure: Virginia doesn't mandate reserve studies for HOAs, but the Virginia Condominium Act requires condominium associations to conduct them and disclose reserve fund status annually.

- Reserve studies identify capital components, estimate useful life and replacement cost, and create a funding plan to avoid special assessments.

- Most boards delay reserve planning to protect homeowners from higher fees—but that delay creates bigger problems later.

- Neighboring states like Maryland, Washington D.C., and North Carolina have stricter requirements than Virginia.

- Without a reserve study, boards make financial decisions blind, often leading to underfunded reserves and emergency assessments.

Overview of Reserve Study Requirements for Virginia HOAs

Virginia HOA Reserve Study Requirements catch most boards off guard: the state doesn't require HOAs to conduct reserve studies. Unlike California, Nevada, or Washington State, Virginia has no statutory mandate forcing homeowners associations to assess long-term capital needs.

Just because something isn't required doesn't mean it's optional if you want to avoid financial disaster. Boards that skip reserve planning face the same outcome—underfunded reserves, deferred maintenance, and special assessments that blindside homeowners.

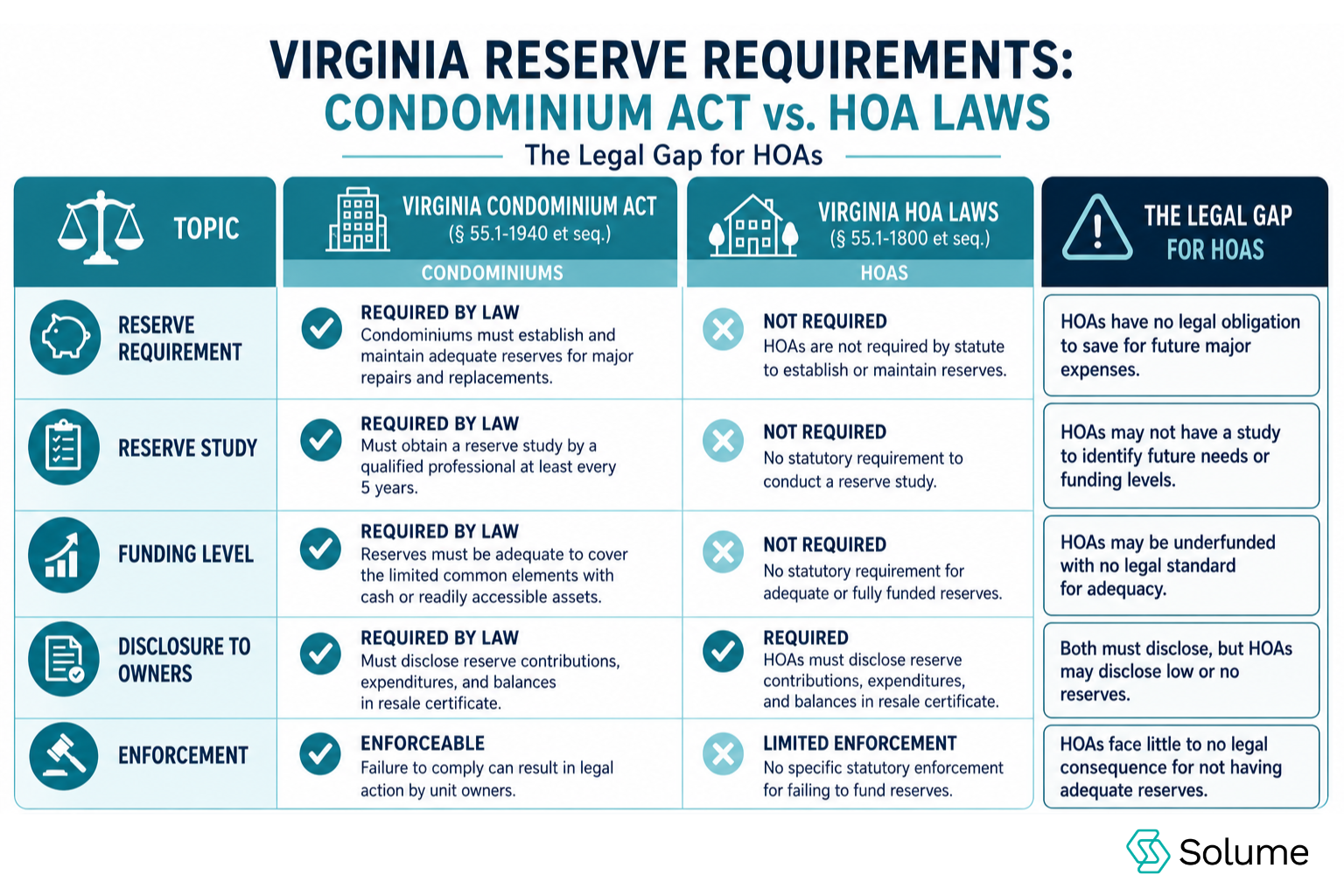

Condominium associations operate under different rules. The Virginia Condominium Act explicitly requires them to prepare reserve studies and disclose reserve fund status to unit owners.

What Is a Reserve Study?

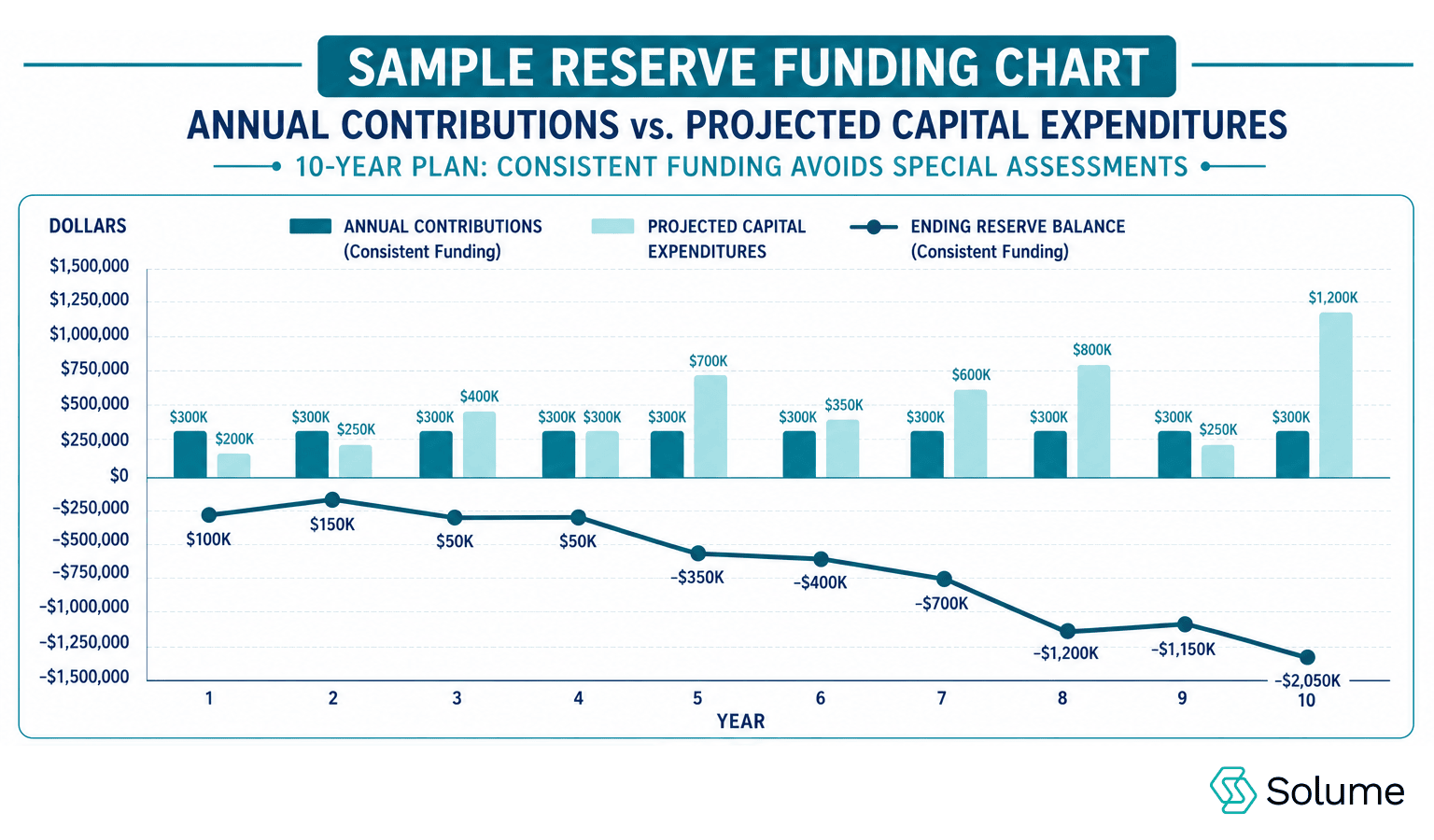

A reserve study is a financial planning tool that identifies all major capital components in your community, estimates their useful life and replacement cost, and creates a funding plan to pay for them without special assessments.

Your roof has 20 years of useful life left. Replacement cost is $150,000. A reserve study tells you how much to set aside each year so the money is there when the roof fails. Without that calculation, boards either ignore the problem or scramble to pass a special assessment when the leak starts.

The study includes two core analyses:

- Physical analysis: An inventory of all common elements—roofs, pavement, pools, fencing, HVAC systems—with condition assessments and estimated useful life remaining.

- Financial analysis: Current amount of reserves, projected capital expenditures, and a funding strategy to meet future obligations.

Small HOAs face the same capital expenditures as large ones. A 30-unit community still needs to replace its parking lot. The difference is that each homeowner carries a larger share of the cost when the reserve account is empty.

Relevant State Laws and Guidelines

The Virginia Condominium Act (§ 55.1-1900 et seq.) governs condominium associations and includes specific reserve study requirements. The board must prepare or update a reserve study at least once every five years and disclose results to unit owners, including current reserves, projected capital expenditures, and expected contribution to replacement reserves.

Virginia HOAs, governed by the Property Owners' Association Act, face no such requirement. The Act doesn't mention reserve studies, reserve funding, or cash reserves. Boards can operate without any formal reserve planning—and many do.

That legal gap creates risk. Without a reserve requirement, volunteer board members often defer reserve contributions to keep dues low. Homeowners appreciate lower fees until the assessment notice arrives.

The Importance of Reserve Studies for Homeowners Associations

Reserve studies answer one question: will your community have enough money to pay for major repairs when they're needed?

Boards delay this question because they're trying to protect homeowners from higher monthly dues. But deferring reserve contributions doesn't eliminate the expense—it shifts the burden to a future board and turns predictable costs into financial emergencies.

Here's what happens without reserve planning:

- The board has no clear picture of future capital expenditures.

- Reserve contributions are arbitrary or nonexistent.

- When a major component fails, the community lacks adequate reserves.

- The board passes a special assessment, often for tens of thousands of dollars.

- Homeowners lose trust, and property values suffer.

Communities that conduct regular reserve studies avoid this cycle. They know which capital components will need replacement, when, and how much to set aside.

How Reserve Studies Impact Association Budgets

A reserve study directly shapes how much your community collects in reserve contributions each fiscal year. The funding plan calculates the gap between your current reserves and future obligations, then spreads that cost across all homeowners.

If your reserve study identifies $500,000 in capital expenditures over the next 10 years and your reserve account holds $100,000, you need to collect $40,000 annually to stay fully funded. That's roughly $275 per month per household for a 100-unit community.

Boards resist these numbers. They see the monthly increase and worry about homeowner backlash. But the alternative is worse: a $50,000 special assessment when the pool equipment fails or the siding needs replacement.

Reserve studies also help boards prioritize capital expenditures. If the physical analysis shows your parking lot has three years of useful life left but your HVAC system has ten, you can prioritize accordingly. Without that data, boards guess—and often guess wrong.

Key Components of a Reserve Study

Every professional reserve study includes two analyses: physical and financial. A physical analysis without financial planning tells you what's broken but not how to pay for it. A financial analysis without a physical inspection is just guesswork.

Physical and Financial Analyses

The physical analysis is a detailed inventory of all common elements the association is responsible for maintaining or replacing. A Reserve Specialist walks the property, documents the condition of each capital component, estimates its remaining useful life, and calculates replacement cost.

Common capital components include roofing systems, paving and sealcoating, exterior painting and siding, pool and spa equipment, fencing and gates, HVAC systems for common areas, and elevators.

Each component gets a condition rating and a timeline. For example, "Asphalt parking lot: fair condition, 4 years remaining useful life, $85,000 replacement cost."

The financial analysis takes that data and builds a funding plan. It starts with the current amount in your reserve account, projects future capital expenditures based on useful life estimates, and calculates the reserve contributions needed to maintain adequate reserves.

The financial analysis also evaluates your funding level. Are you fully funded (100% of required reserves), partially funded (50–70%), or critically underfunded (below 30%)? This metric tells you how much risk your community carries.

Role of a Reserve Study Professional

Most boards lack the expertise to conduct a reserve study themselves. Reserve study professionals bring specialized knowledge of construction costs, useful life data, and funding strategies. A qualified Reserve Specialist typically holds a credential such as RS (Reserve Specialist) or PRA (Professional Reserve Analyst) from organizations like the Community Associations Institute (CAI).

The Reserve Specialist's job is to assess your property objectively and deliver a funding plan that reflects reality—not what the board hopes to hear. If your community is underfunded, they'll tell you. If your funding strategy defers too much cost to future years, they'll flag it.

Boards should update reserve studies every three to five years. Capital components age, replacement costs change, and funding strategies need adjustment.

State-Specific Considerations for Reserve Studies

Virginia's lack of reserve study requirements for HOAs stands out when you compare it to neighboring states. Several states in the region have moved toward mandatory reserve planning, especially for condominium associations.

Neighboring States' Requirements

Maryland: Condominium associations must prepare a reserve study at least once every five years and disclose results to unit owners.

Washington D.C.: Condominium associations are required to conduct reserve studies and maintain replacement reserves. The board must review the reserve account annually.

North Carolina: Condominium associations must prepare a reserve study and disclose reserve fund status to unit owners.

West Virginia: Similar to Virginia, West Virginia doesn't mandate reserve studies for HOAs but requires condominium associations to maintain replacement reserves.

How Virginia Differs

Virginia Condominium Act requirements are clear: condominium associations must conduct reserve studies, disclose reserve fund status, and maintain replacement reserves. But Virginia HOAs work in a legal gray zone. The Property Owners' Association Act doesn't require reserve planning, leaving the decision entirely to the HOA board.

This creates a split in how Virginia communities approach reserve funding. Condominium associations follow state laws and generally maintain adequate reserves. HOAs often underfund reserves or skip reserve planning altogether—not because board members are irresponsible, but because they lack a legal mandate and face pressure to keep dues low.

The risk is that boards assume "no legal requirement" means "not necessary." In reality, capital components don't care about state laws. Your roof will fail whether you planned for it or not. The question is whether your community will have the cash reserves to pay for it without a special assessment.

Final Notes on Virginia HOA Reserve Study Requirements

Virginia HO Reserve Study Requirements don't exist for HOAs, but that doesn't make reserve planning optional if you want financial stability. Boards that skip reserve studies face the same problems: underfunded reserves, deferred maintenance, and special assessments that damage community trust.

Condominium associations in Virginia must follow the Virginia Condominium Act and conduct reserve studies at least every five years. If your community is structured as a condo association, this isn't a recommendation—it's a legal obligation.

For HOAs, reserve planning is a choice. But it's the difference between a board that manages capital expenditures strategically and one that reacts to emergencies. Reserve studies give you the data to make informed decisions about reserve contributions, funding strategies, and long-term financial management.

If your board needs clearer reserve planning and wants to avoid special assessments, explore your options with a 15-minute call to see if Solume fits your community.

Frequently Asked Questions

Are reserve studies required for HOAs in Virginia?

No. Virginia state laws don't require homeowners associations to conduct reserve studies. However, condominium associations must prepare reserve studies under the Virginia Condominium Act and disclose reserve fund status to unit owners.

How often should a reserve study be updated?

Most reserve study professionals recommend updating every three to five years. Capital components age, replacement costs change, and your funding plan needs adjustment to stay accurate. The Virginia Condominium Act requires condominium associations to update reserve studies at least once every five years.

What happens if an HOA doesn't have a reserve study?

The board operates without a clear picture of future capital expenditures. Reserve contributions are often arbitrary or insufficient, leading to underfunded reserves. When major repairs come due, the community typically passes a special assessment to cover the cost.

Can a board waive reserve contributions?

Technically, yes—but it's a terrible idea. Waiving reserve contributions might keep dues low in the short term, but it guarantees special assessments later. Capital components will fail whether you fund reserves or not. The only question is whether you'll pay for them gradually or all at once.

How much should an HOA keep in reserves?

That depends on your capital components, their useful life, and replacement cost. A reserve study calculates the exact amount. As a general rule, communities should aim for at least 70% funded reserves. Anything below 30% is critically underfunded and puts the community at high risk for special assessments.

Do small HOAs need reserve studies?

Yes. Small communities face the same capital expenditures as large ones—roofs, pavement, fencing, and major repairs don't cost less just because your HOA has fewer units. In fact, small HOAs carry higher risk because each homeowner shoulders a larger share of the cost when reserves run out.

What's the difference between a reserve study and a reserve fund?

A reserve study is the analysis that identifies capital components, estimates useful life and replacement cost, and creates a funding plan. A reserve fund is the actual money set aside to pay for those future expenses. You need both—the study tells you how much to save, and the fund holds the money.

Is a reserve study worth the cost if we're a small community?

Yes. The cost of a reserve study—typically $2,000 to $5,000—is minimal compared to the cost of an unexpected $50,000 special assessment. Small communities actually benefit more from reserve studies because each homeowner carries a larger financial burden when reserves run out. The study gives you a roadmap to spread that cost over time instead of hitting everyone at once.