A 12-unit condo association in Florida found $4,000 in its reserve account the same week a structural engineer flagged $90,000 in needed concrete repairs. The board hadn't kept real books for three years. They had a checkbook register and a hope that things were fine. That gap between what they thought they had and what they actually had is exactly why Bookkeeping for small HOAs matters. This guide walks through how to set it up properly, from the first bank account to the software decision.

Key Takeaways

- Bookkeeping for a small HOA means systematically recording every dues payment, assessment, and vendor expense so the board can see the community's true financial health.

- Fund accounting sets HOAs apart from businesses by requiring the strict separation of operating and reserve funds to prevent commingling and compliance violations.

- Separate bank accounts and a clear chart of accounts are the foundation of accurate, transparent HOA financial management.

- Self-managing the books is practical for small communities, but as communities grow, stricter state laws and the cost of errors often make dedicated tools worth it.

Financial responsibilities and core bookkeeping duties of a small HOA

The financial responsibilities of a board come down to one principle. Every dollar that enters or leaves the community has to be tracked, categorized, and explained to any homeowner who asks. For a small HOA, that means recording dues, posting payments, reconciling monthly, and producing readable financial reporting. This is a core board responsibility, not optional paperwork. It proves the board is meeting its fiduciary duty. The same small-organization bookkeeping fundamentals that apply to any nonprofit or small entity also apply to HOA bookkeeping here.

The reason this matters is legal as much as practical. Board members hold a fiduciary responsibility to homeowners. Sloppy Bookkeeping for Small HOA work is one of the fastest ways to breach it. Core duties include managing accounts receivable, handling accounts payable, monitoring cash flow, and tracking reserves separately. Solid HOA financial management tools make these duties easier to handle. Many assume these tasks only matter for large communities. In reality, a self-managed homeowners association with 20 units carries the same legal obligations as one with 2,000.

Common bookkeeping challenges and pitfalls for small/self-managed HOAs

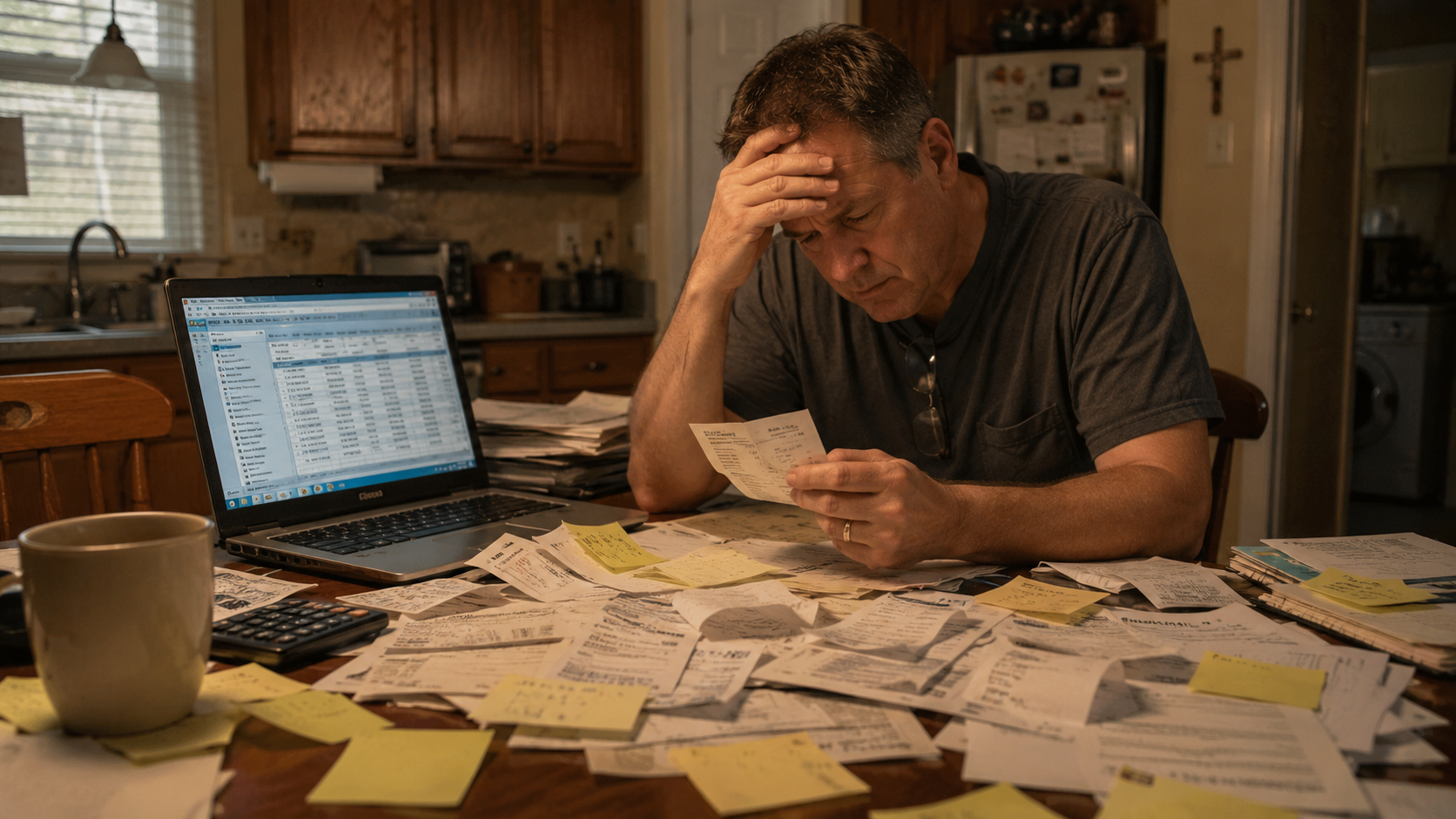

Here's the hard truth: most small HOA bookkeeping failures come from volunteer board members doing their honest best with the wrong tools. Someone tracks dues in a spreadsheet, someone else holds the checkbook, and nobody reconciles anything until tax season. Then a payment goes missing, and trust evaporates. If you want a deeper walkthrough, our guide on improving financial management for a small HOA covers these failure points in detail.

The most common pitfall is commingling operating and reserve money in a single account. What actually happens is the board spends reserve funds on a routine repair because the cash was sitting right there. Suddenly, the long-term plan is underfunded. Other problems include inconsistent dues collection, no assessment process, missed reconciliation, and late financial reporting. Board turnover makes it worse. Knowledge walks out the door when a treasurer resigns.

State compliance requirements add real pressure, and tax deadlines compound it. Associations also need to understand how their filings work, such as IRS Form 1120-H for homeowners' associations, which has its own eligibility and reporting rules. After the 2021 Surfside collapse, Florida tightened reserve and inspection rules. The Miami-Dade County government documented that tragedy in detail. The rules governing Bookkeeping for Small HOA communities vary by state, so check your governing documents and confirm requirements with your state's HOA statute or a qualified professional.

Managing expenses, vendor payments, and accounts payable

Operating expenses are where small communities quietly bleed money. Landscaping, insurance, utilities, pool service, minor repairs: each is small on its own. But without a clean accounts payable process, they add up to a budget no one understands. Every vendor payment should be tied to an invoice, approved by the right person, and posted to the correct category in your chart of accounts.

Most boards assume tracking vendor payments is just paying bills on time. It is more than that. You need a record of who approved each payment, what it was for, and which fund it came from. That paper trail protects the board if a homeowner questions a $3,000 check or if an auditor reviews the books. Following recognized accounting standards from the AICPA gives that trail real credibility. Set a simple rule: no payment goes out without a matching invoice and a second set of eyes.

Vendor management also feeds your budgeting. When accounts payable is organized by category, you can see exactly what the landscaping cost was last year versus this year. That makes the annual budget far more honest. Solume centralizes vendor management and tracks expenses by category, so a self-managed HOA can keep payments organized without juggling separate files and spreadsheets.

Budgeting and annual budget preparation

A good annual budget is just last year's real numbers plus what you know is coming. The mistake small boards make is building the budget on guesses rather than on actual financial reporting. If your HOA finances are clean, budgeting becomes mostly arithmetic. If they aren't, you're guessing, and guesses are how communities end up with special assessments. Working from a step-by-step HOA budget template keeps the process grounded in real figures.

Start with your operating expenses by category, pull the actual spending from the prior year, and adjust for known increases, such as insurance premiums or a new service contract. Then add the reserve fund contribution, which is not optional money left over at the end. It is a line item funded first. Build the budget so dues cover both operating costs and the reserve allocation your reserve study calls for.

The root cause of most underfunded communities is a board that sets dues to keep them low rather than to cover real costs. That feels generous to homeowners in year one. By year five, deferred maintenance has piled up, and the bill comes due all at once. Honest budgeting protects homeowners better than artificially low dues ever could.

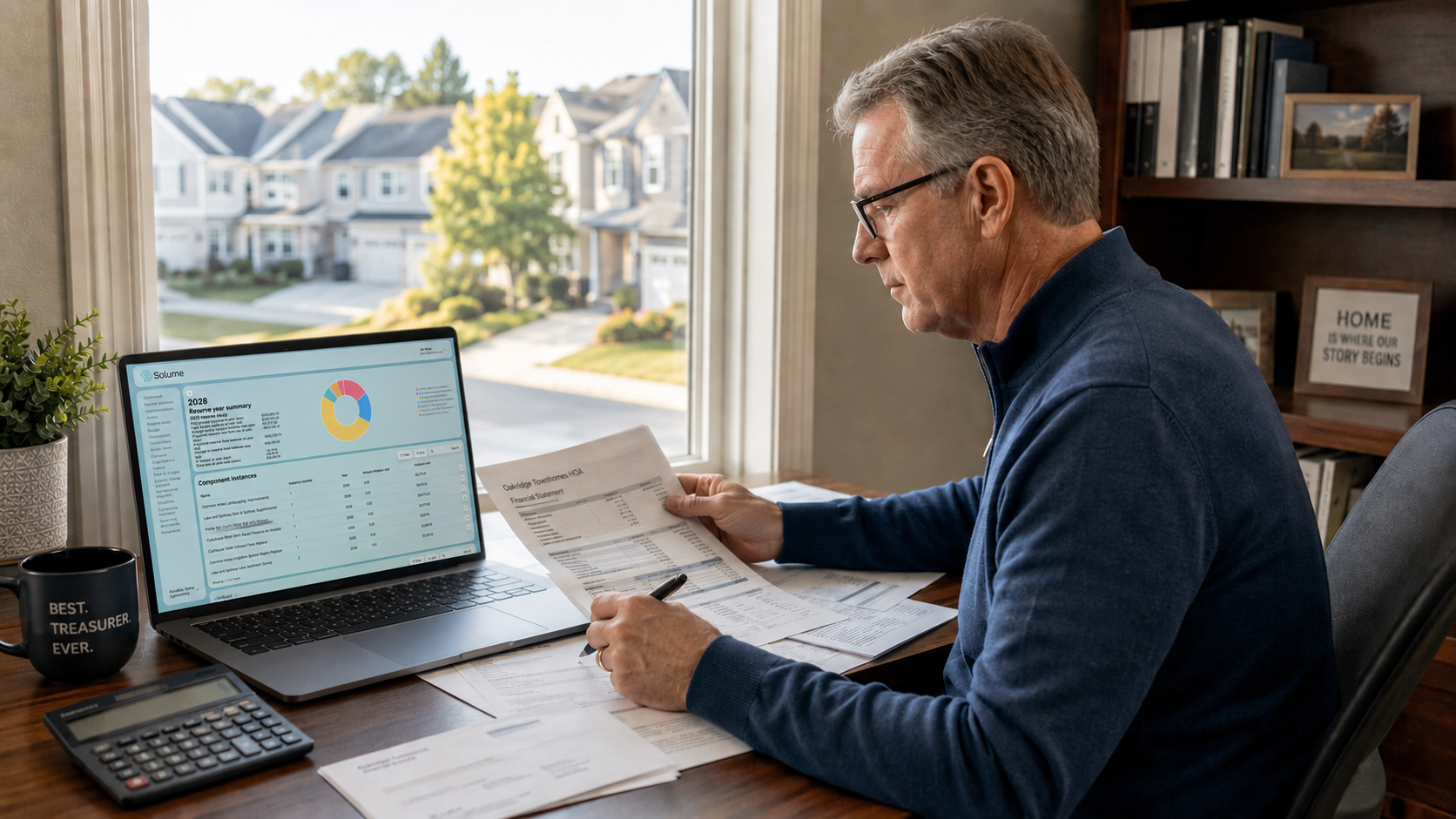

Reserve fund management and reserve planning

The reserve fund is the money set aside for big-ticket repairs and replacements: roofs, roads, elevators, pool resurfacing. Reserve planning is the discipline of knowing what those components will cost, when they'll fail, and how much to set aside each year. The goal is simple: the money exists when you need it. This is the single biggest gap in the finances of small HOAs.

What many communities don't realize is that a reserve study isn't a one-time document you file and forget. It is the foundation of every day-to-day and long-term planning decision you make. The study tells you, component by component, the funding target. Keeping reserve contributions flowing into a separate account that is never used for operating costs is a fundamental board responsibility.

The risk most boards overlook is the timing mismatch between when components fail and when funds are available. A roof doesn't wait for the reserve balance to catch up. States like Florida, Nevada, and California now mandate reserve studies and funding for many associations. Because the reserve study requirements by state vary so widely, verify your obligations with your state statute or a reserve professional. Underfunded reserves are the direct path to surprise special assessments.

Choosing HOA bookkeeping/accounting software or services

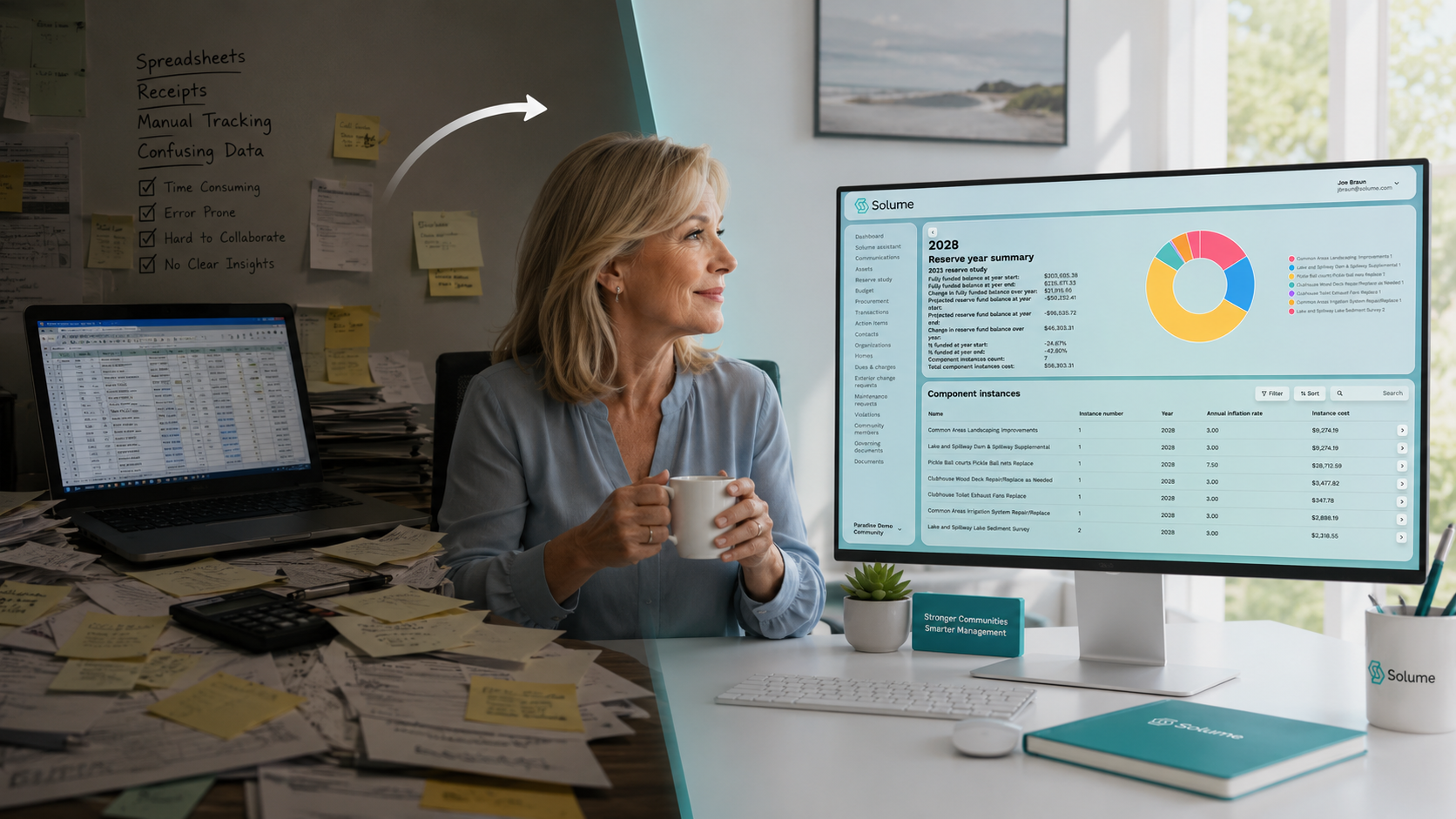

You have three real options for Bookkeeping for a small HOA. You can keep doing it manually, use general accounting software like QuickBooks, or use a platform built for community associations. General business software handles the debits and credits fine. But it doesn't understand fund accounting, reserve tracking, or assessment management out of the box. You end up forcing HOA logic into a tool that wasn't designed for it.

HOA accounting software built for associations tracks operating and reserve funds separately, automates dues collection, generates reporting, and keeps an audit trail homeowners can trust. The right HOA accounting software also flags delinquent accounts receivable and supports tax compliance. An automated dues collection system replaces hours of volunteer labor and reduces manual-entry errors for a self-managed HOA.

A professional bookkeeping service is the other path, useful when no board member has the time or skill. Solume was built specifically for self-managed communities. It combines financial management, automated reserve study tools, and dues collection in one place, so boards aren't stitching together separate systems. Compare what each tool does against what your community actually needs before committing.

Fraud prevention and financial controls in small HOAs

Small HOAs are surprisingly easy targets for fraud, precisely because everyone trusts everyone. One person controls the checkbook, signs the checks, and reconciles the account. That's not a system; that's an invitation. Fraud prevention starts with separating those duties and protecting cash flow.

The reason this matters is structural. When a single person can both authorize and record a payment, there's no second check on where the money goes. A few basic controls close that gap. Require two signatures on checks above a threshold. Have someone who doesn't write checks review the bank reconciliation each month. Distribute financial reports to the full board so that more than one volunteer board member can see the numbers.

Financial transparency is itself a control. When homeowners and the board can see the books, theft becomes harder to hide and easier to catch early. A condo association accounting setup that produces clear, regular reporting protects the board as much as the community. A professional bookkeeping service can build those controls in from day one. The point isn't to assume the worst of volunteers. It is to make sure no single point of failure can drain the community's funds.

Transitioning from spreadsheets to dedicated HOA software

Moving from spreadsheets to software feels like a hassle, which is why boards put it off for years. But the spreadsheet that worked for 10 units quietly breaks at 40. The day it breaks is usually the day a number turns out to be wrong in a way that costs the community real money.

The transition is more manageable than most boards expect. Start by closing out your current fiscal period in the spreadsheet so you have clean ending balances. Set up your chart of accounts in the new system, enter opening balances for both operating and reserve funds, then import or re-key the homeowner roster and dues records. Run both systems in parallel for one month to confirm the numbers match. If you want to keep learning, we publish more HOA accounting resources that cover each of these steps in more depth.

The payoff is dependable HOA accounting software you can trust. Once dues collection, vendor payments, and reporting live in one place, statements generate themselves. The HOA finances stay visible, financial transparency holds, and bank reconciliation takes minutes instead of an afternoon. The spreadsheet era ends, and so does the constant fear that something was missed.

If your board wants a clearer way to handle Bookkeeping for a small HOA, reserve planning, and vendor oversight without depending on a management company, it may be worth seeing whether the right tools fit your community. You can book a 15-minute call to see if Solume is a good fit and walk through how it handles the bookkeeping work your volunteers are doing by hand today.

Frequently Asked Questions

What exactly does bookkeeping for a small HOA involve?

It's the process of recording, classifying, and tracking every financial transaction in your association, from homeowner dues and assessments to vendor payments and bank reconciliations. The goal is to keep the books balanced so your board can clearly see the community's financial health and stay compliant with state reporting rules.

How is HOA bookkeeping different from regular small business bookkeeping?

HOAs use fund accounting, meaning you track two separate pots of money:an operating fund for daily expenses and a reserve fund for long-term projects, and you can't commingle them. Unlike a business that earns income from sales, an HOA relies almost entirely on member dues and assessments, so monitoring payments and delinquencies becomes a central task.

What's the best accounting method for a small HOA, cash or accrual?

Cash basis records money when it actually changes hands and is simpler for volunteer boards, while accrual records income and expenses when they're earned or incurred and gives a more accurate picture of obligations. Many states require accrual or modified accrual for official reporting, so check your governing documents and state law before making a choice.

Should a small HOA hire a bookkeeper or handle it themselves?

If your board has members with financial skills and time to handle dues collection, reconciliations, and reporting, self-management is realistic for smaller communities with few units. As the community grows or compliance becomes more complex, the workload often exceeds what a volunteer can reliably manage, at which point software or outside help becomes worth it.

What happens if our HOA commingles operating and reserve funds?

Commingling blurs the line between how much money is genuinely available for daily operations and long-term repairs, which can lead to underfunded reserves and surprise special assessments. In many states, it's also a compliance violation that exposes the board to fiduciary liability, so keeping separate bank accounts is a basic safeguard, not an optional one.

How do we set up bookkeeping for our HOA from scratch?

Start by opening separate bank accounts for operating and reserve funds, then build a chart of accounts that categorizes all types of income and expenses your community has. From there, set a consistent schedule for recording transactions, reconciling them against bank statements, and producing financial reports for the board to review.